Seven is a special number. Be it Mathematics (Prime Numbers and Number Theory), Music (seven musical notes), Astronomy (days in a lunar phase) or Mythology (Sapta Chakra, Sapta Samudra or Sapta Rishi), the cycle of sevens is a constant around us.

It is apt then that, as the Goods & Services Tax (GST) turns seven this month, we take a moment to examine how GST, arguably the biggest tax reform since Independence has fared since it was rung-in at midnight on the 1st of July, 2017.

Since then, GST has received considerable academic attention. Every facet from the simplification of compliances, improvements in logistics to robust revenue collections have all been examined at length.

Amongst the many perspectives on GST, one has been the recent discussions on the revenue performance of GST indicating, inter alia, that while Gross Revenue Collections have been surging, Net Revenues have not kept pace and have only recently reached pre-GST levels. This slippage in net collections has been viewed with some consternation. Further, some concerns have been raised on the lack of availability of data especially on refunds as well as on the working of the GST Council. Let us delve deeper into each of these points beginning with revenue performance.

The Revenue Relish

There has been considerable analysis of revenue collections under GST. While, there is little dispute regarding the robustness of gross revenue yields, however in order to address the concerns raised about net GST collections i.e. revenue collections net of refunds [primarily on account of exports], we delve a bit deeper into the numbers.

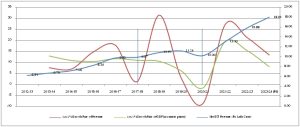

We base our examination on GST collections as reported in the Budget documents. This is then compared against the pre-GST revenue collections for taxes subsumed in GST for both the States as well as the Centre. The results are plotted as under (Figure 1, Right Axis).We also plot the year-on-year growth of GST collections as well as the year-on-year growth in GDP (Figure 1, Left Axis).

Fig. 1: Net GST Revenue [Right Axis] v. Y-o-Y Growth in GDP and in Revenue Collections [Left Axis

| GST Introduced |

| Covid, Wave I & II |

From the above, we can see three things. Firstly, net revenue collections have been on a steady uptick and that the pace of growth has increased post introduction of GST; secondly, the year-on-year growth of net revenue averaged 12.76% in the post-GST period (as against 11.81% in the pre-GST period), this is despite the exogenous shock of the pandemic; thirdly, we can see that net revenue growth has consistently outperformed GDP growth. This is reflective of systemic efficiencies in the new tax regime.

Amongst other variables, revenue collections are a function of the tax rates. For context, we may recall that, the improvement in tax collection efficiencies was accompanied by a significant reduction in tax rates. In the run-up to the introduction of GST, the Committee on the Revenue Neutral Rate (RNR) for GST had recommended a rate of 15-15.5%.

As against this at the time of introduction, the effective GST rate was estimated as being 14.4%. This was subsequently reduced to 11.6% in September 2019[1] and stood at 12.2% in March, 2023. In revenue terms, this can be quantified as a saving [stimulus?] for the economy in excess of Rs. 4.3 Lakh Crore in just the last year! It is interesting to note that comparing internationally; India’s GST Rates are amongst the lowest in the world (Figure 2).

Fig. 2: Comparing Standard Consumption Tax (VAT/GST) Rates across select OECD countries

Tax Buoyancy: A robust measure of tax efficiency

A rising tide raises all boats. Revenue growth is a natural corollary of a growing economy, however the growth (or buoyancy) of revenue collections over and above the growth in GDP is the real test of the systemic efficiencies of a tax system.

On this account, in the five years prior to the introduction of GST, the net revenue buoyancy vis-à-vis GDP (at current prices) stood at 1.02 whereas it was 1.28 in the seven years post-GST. This is a testament to the collection efficiencies brought to the fore by GST.

Infact, India’s GST collection efficiency [the percentage collected out of the maximum possible tax – presuming perfect compliance and coverage across all consumption] stood at 0.61 in 2022-23. For context, comparing it against that of the 37 OECD countries sees India placed in the top one-third (Figure 3).

Fig. 3: Comparing C-efficiency for consumption Taxes (VAT/GST) across selected OECD countries

A question of Data

Admittedly, the revenue figures released on a monthly basis have typically featured Gross collection figures. Net figures have been published only since February, 2024. However, annual statistical reports for each year since the introduction of GST have been published and placed in the public domain. These reports feature month-wise details relating to the GST refunds on account of exports. Therefore public visibility to refund data, although with a lag, has been there.

We move on to examine the averment, without any basis, that the GST Council is “dominated” by the Centre. With the introduction of GST, the Centre and the States, pooled their sovereignty in matters related to administration of the new tax especially in areas such as policy making, fixation of rates, drafting of laws/rules, co-ordinating compliances etc. This is at times cited as a restriction on the powers of the States. However, it is equally a “restriction” for the Central Government.

The GST Council, supported by its Committees has delved into a number of complex issues and has come up with recommendations which have brought about symmetry in the administration of the law and stability in the rate structure.

It is a testament to the spirit of co-operative federalism that save one, all decisions of the GST Council have been taken by consensus. Moreover, all decisions of the Council for improving compliance plugging loopholes or rationalizing exemptions have benefited the Centre and the States equally.

From the above discussion, three points emerge – firstly, the collection efficiencies of GST are apparent, consistent, ab-initio and are primarily on account of endogenous factors – this holds even when we look at revenue collections net of refunds; secondly, our tax rates as well as our collection efficiencies compare favourably with the rest of the world; thirdly, GST has delivered consistent revenue growth even at lower tax rates and in the face of external shocks.

As GST moves to its next phase of growth, there are a number of areas that will need to be addressed such as simplification of the rate structure, inclusion of items left out of GST as well as administrative issues such an efficient appellate mechanism, however as GST turns seven there is much to celebrate.

(The author is an Indian Revenue Service officer of the 2007 Batch. Views presented are his own. Courtesy; PIB)